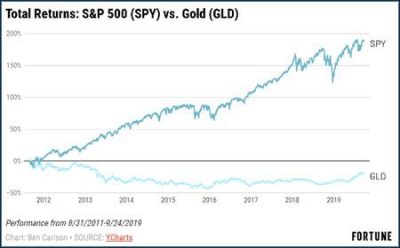

A recent article in Fortune presents a cautionary tale about performance chasing by citing the example of the SPDR Gold Shares ETF’s (GLD) performance over the last decade.

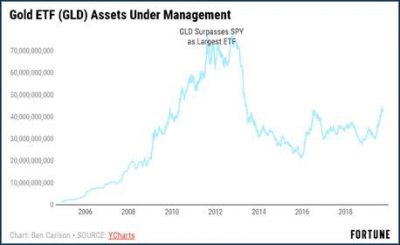

“From a high of more than $77 billion in that late-summer of 2011, assets under management (AUM) in GLD fell all the way to $21 billion by the end of 2015. What’s interesting in this scenario is how much more AUM fell than performance in the underlying fund.”

The article explains: “Some of this could have been due to the fact that the financial crisis created a flight to hedge systematic risk, of which gold is a favored proxy for many. But it’s clear there was also an element of performance chasing going on as well.” After the 2008 crash, it adds, investors were “eager for alternative investments that would either hedge the stock market or offer an uncorrelated return stream with high expected returns.”

Performance chasing is “as old as the hills” the article concludes, adding, “so this type of behavior is never going away.” The problem, however, is that “most investors tend to put their money into these strategies only after they’ve already experienced strong outperformance.”