By Jack Forehand —

When we started managing money, I used to focus on what I knew.

Today, after over 12 years doing it, I have learned it is best to focus on what I don’t know because no matter how much you learn in this business, what you don’t know will always far exceed what you do.

Looking back on everything I’ve learned, I’m pleased to say that the principles I initially believed have proven to be mostly correct. These include; following factor-based strategies with strong historical track records, focusing on the long-term and eliminating emotion from the investing process, all of which have proven to be successful. But the application of those principles is a very nuanced process, and the introduction of investor behavior into the equation can make things even more complicated.

While it would be impossible to document all the knowledge I’ve gathered in over a decade of managing money, I thought it might be interesting to take a look at a few major lessons:

Lesson #1: You Can Beat the Market, But 95% of Investors Won’t

There is no question that, in the aggregate, active management will trail the market. Academic research has proven that the portfolios of active managers will be the same as the market, and will therefore produce the same returns with higher fees and trading costs. In the long-run, when compared to an index fund, the underperformance of active managers will more or less equal the sum of excess fees and excess trading costs.

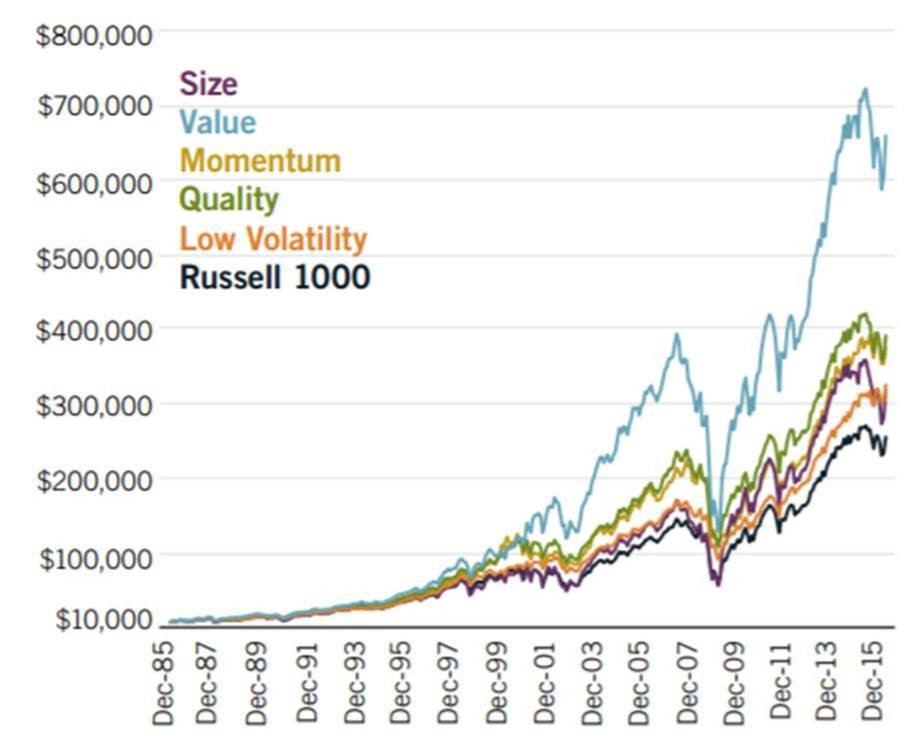

Despite this fact, however, there is strong evidence suggesting that factor-based strategies, when followed with discipline, present investors with excellent long-term potential to outperform the market. Firms like AQR, Research Affiliates and O’Shaughnessy Asset Management have published many research studies that show this (the chart below, using data from Fidelity, shows that stocks with certain factor characteristics have exhibited outperformance). Testing we conducted prior to starting our money management business supports this thesis, but it’s important to consider how fees, transaction costs and the natural cyclicality of investing styles can detract from real world returns. We have found that the outperformance potential of factor- based strategies does persist in the real world, with the major caveat that to achieve this outperformance, you have to stick with such strategies through extended periods of inevitable underperformance– which can be very difficult for investors to do.

Lesson #2: Crises Are Much Worse Than You Think – And You Can’t Back-Test Pain

I started in money management right after the 2000 bear market. Having worked for an Internet-based company during the dotcom crash, I certainly had a grasp for the severity of bear markets and how quickly things can change when they occur.

Having studied past bear markets and other investing crises, I knew that the market always comes back, even from the most severe declines. I compiled the results from past bear markets when I developed our investment strategies and felt confident in the performance parameters I had established.

And then 2008 happened.

When living through a financial crisis, one of the first things you learn is that there is no way to model or quantify what it feels like. The complete loss of optimism for the future feels like an overwhelming weight on the market and the economy. Everyone seems to feel that this time will be different and we will never come back and, while you know that isn’t true, the direness of the situation tests even the strongest convictions . I don’t think it’s possible to fully understand that until you have lived through such a period with real money on the line – whether it be client money or your own.

The pain those losses cause for investors will test even the most carefully thought-out investing strategies. When running tests of investment models, it is easy to look at periods of loss as a blip on the radar in the context of the long-term, especially since bear markets inevitably end and the market goes on to set new highs. The chart below shows bull and bear markets since 1903, courtesy of Newfound Research.

The data clearly shows how much longer and greater in magnitude bull markets are, and it’s very easy to have confidence that things will work out in the long-term when you are armed with historical results to back up your investment process. But those results don’t incorporate what is probably the most important factor with respect to actual results – investor behavior.

In the process of developing a risk profile for a new client, the vast majority will tell you that they will stay the course if the market goes down, but many will not actually do it. So the experience of managing client money during a decline teaches you that it isn’t done in a vacuum. If you have a strategy that works great over the long-term, but investors can’t stick with it when things get bad, then you won’t achieve your long-term objectives.

Lesson #3: Underperformance Can Be Worse Than Market Losses

When you study active management, one of the first conclusions you draw is that to beat the market, you have to be different. This concept of how different your portfolio is from the market is called active share and, although evidence is mixed on the subject, data suggests that portfolios with a high degree of active share stand a much better chance of outperforming than closet indexers, who also generally charge higher fees than the market but have portfolios that look very similar to it.

So, it seems quite simple in theory: build a portfolio that follows principles that work over time, have the conviction to look different from the market, and you have a good chance to outperform. The fly in the ointment, however, is that this approach could lead to returns that also deviate from the market, sometimes by a wide margin.

This is where the true test of active management comes in, one that is also deeply rooted in investor behavior. Although many investors will panic and sell when the market goes down, there is at least an understanding that losses should be expected during a market decline since even index investors will be losing money. When performance is not keeping up with those index funds, though, things can really get tough.

Through the years, I have found that it is more likely for investors to abandon a strategy because of underperformance than because of losses. This is especially true if they experience a situation where an investment strategy is down in a year where the market is up, as many deep value strategies have been in recent years.

If a money manager uses an active strategy, and charges higher fees than index funds, then they will go through periods of charging clients higher fees to underperform the market. While it is a necessary evil to beat the market over time, this can be incredibly challenging to deal with when it is happening. It can also lead investors to abandon strategies at the absolute worst time. We have learned how to better deal with this and to encourage more prudent behavior when it happens (which is a topic for a future article), but it is an uphill battle, to say the very least.

Recognizing the Limits of Your Own Knowledge

I’m certain that, in ten years’ time, I will have many more lessons to share. That is the nature of investing–no matter how much you know, it will always pale in comparison to what you don’t. As we strive to become better investors, that may be the greatest lesson of all.

If you would like a notification when future posts are released, you can follow me on twitter at @practicalquant.

Photo: Copyright: convisum / 123RF Stock Photo

Jack Forehand is Co-Founder and President at Validea Capital. He is also a partner at Validea.com and co-authored “The Guru Investor: How to Beat the Market Using History’s Best Investment Strategies”. Jack holds the Chartered Financial Analyst designation from the CFA Institute. Follow him on Twitter at @practicalquant.