By Justin J. Carbonneau (@jjcarbonneau) —

In 2005, Joel Greenblatt, a successful hedge fund manager, published an incredibly simple book on disciplined value investing. The book, The Little Book that Beats the Market, went on to be a best seller. In the book, Greenblatt developed a method that sought to combine Ben Graham’s deep value stock selection approach with that of Warren Buffett, who is mostly known for buying high quality and profitable companies at sensible prices. Greenblatt created a stock screening strategy he called the Magic Formula. It was the intersection of these two principles (value + high quality/profitability), achieved through a ranking system that showed significant outperformance over the market in a back-test Greenblatt published in his book.

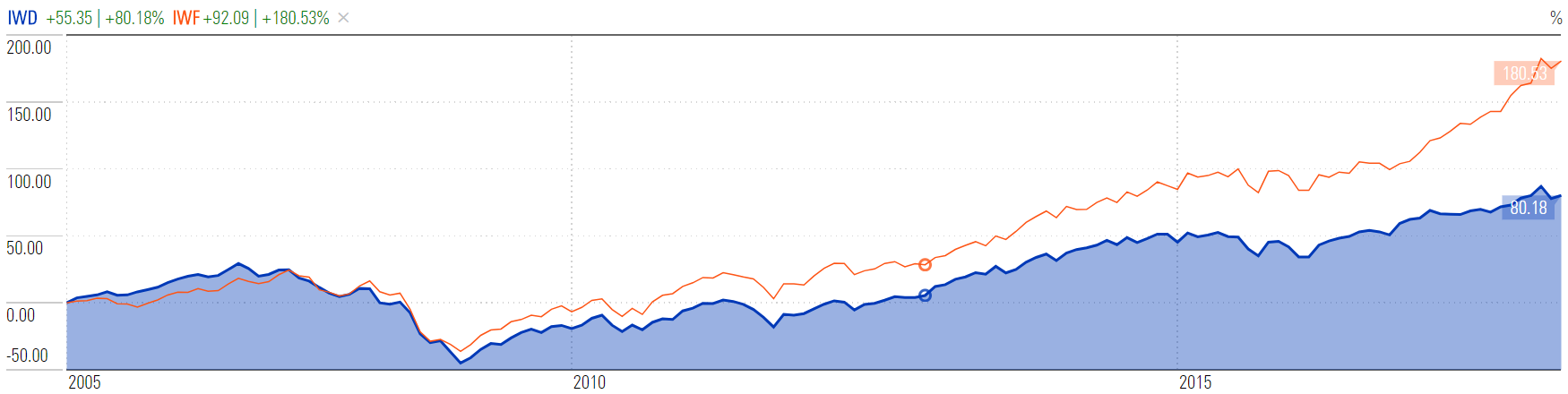

It’s funny how things work out though, because since the publication of Greenblatt’s book, value stocks, by most measures have underperformed growth stocks. Looking at the Russell 1000 Value and Growth ETFs, we can see the performance difference in the chart below going back to Dec. 2005. But what if you were able to isolate the deepest of deep value stocks? Could that have done better over the long-term, and could it produce performance above and beyond that of the Magic Formula. Will value stock performance eventually revert and start to show improved relative performance? Those are some of the questions that Tobias Carlisle helps answer in his book, The Acquirer’s Multiple: How the Billionaire Contrarians of Deep Value Beat the Market.

Over the past few years, Carlisle has emerged as an authority on systematic deep value investing. He is the author of multiple books, including Quantitative Value with Wes Gray (CEO of Alpha Architect) and Deep Value, and runs his own money management firm, Carbon Beach Asset Management. He has a popular investing blog on the Acquirer’s Multiple web site and offers both free and premium stock screens using his quantitative model. Carlisle has done a number of podcasts recently, including a good one with The Investors Podcast.

What Would a Buyer Pay?

As investors, we’ve been trained to pay most attention to a company’s market capitalization to determine its value. The market cap, for short, is the value investors are putting on the company in the public markets.

If you were to buy a company outright today in a private transaction, however, you would also have to look at other things. For instance, how much debt does the firm carry? Once you purchase the company, that debt will need to be paid back. On the flip side, how much cash does the company have on hand? Once you own the firm the cash is yours.

One of the most important lessons Ben Graham tried to teach us in The Intelligent Investor that as investors we should be acting like owners, so if you are going to buy a business, you want to arrive at an accurate and reasonable valuation for it, including debt, cash and other items that will influence the price that you pay.

This is where Carlisle picks it up.

Enter the Acquirer’s Multiple

Carlisle first starts out by asking, how much would a private buyer pay for a company? This is the enterprise value of the firm. To determine the enterprise value, he takes the market cap of the stock, adds back in preferred equity, minority interest and debt. Debt would need to be paid back by a buyer in any takeover, while cash on the balance sheet would immediately be available to the buyer – the enterprise value takes care of these adjustments. The enterprise value gives us a better sense of what a buyer might value the company at before any premium is applied to the purchase price.

The next step is to determine the firm’s operating earnings. By looking at operating earnings, you get a clear picture of the earnings being generated from the actual business. One-time adjustments are excluded from operating earnings. Furthermore, operating earnings don’t include interest expenses or taxes. So the operating earnings calculation acts as a way to standardize the earnings and compare companies with different capital structures.

The ratio of the enterprise value to operating earnings is what Carlisle calls the Acquirer’s Multiple. The lower the number, the better and more attractive.

| Enterprise Value = + Market Value of Common Stock + Market value of preferred equity + Market value of debt + Minority interest – Cash and investments |

|

Operating Earnings = Top-line Revenue – Cost of goods sold + Selling, general and administrative costs + Depreciation and amortization |

|

|

||

Margin of Safety and Mean Reversion

By selecting stocks using the Acquirer’s Multiple, an investor takes advantage of two very important and tested concepts. The first is buying stocks that have a “margin of safety”. The margin of safety was one of Ben Graham’s core investment principles. By purchasing stocks at or below their true value an investor will have a margin of safety in that if they are wrong about their investment thesis, losses should be minimized. The second is mean reversion, which is the concept of things reverting to their historical average. Take the chart above on value vs. growth stocks, mean reversion would argue that the long current period of growth outperformance sets the stage for better relative performance for value going forward. With individual companies, it’s the same concept in that if a firms business is temporarily beaten down, say due to cyclical or transitory factors, a good business with earnings power will recover and revert back to normal.

In his book, Carlisle links margin of safety and mean reversion together with the following quote:

“A wide margin of safety is important because it gives mean reversion time to work its magic.”

He fleshed this out in an interview on Abnormal Returns, where he boils margin of safety and mean reversion in the following three rules.

“Margin of safety is chiefly found in the discount to value. But it is also a test of the balance sheet and the business. My three rules are:

- The greater the company’s discount to its value, the bigger the margin of safety. A wide discount allows for the ordinary errors in calculations of value. And it allows for any drop in value.

- Make sure the company is solvent and liquid. Many, many businesses have been killed by too much debt.

- Make sure the company owns a real business with historically strong operating earnings with matching cash flow. Companies that own science experiments, or toys in search of a business model are for speculators. But weak current profits in a stock with a good past record creates a good chance for mean reversion.”

Long Term Performance

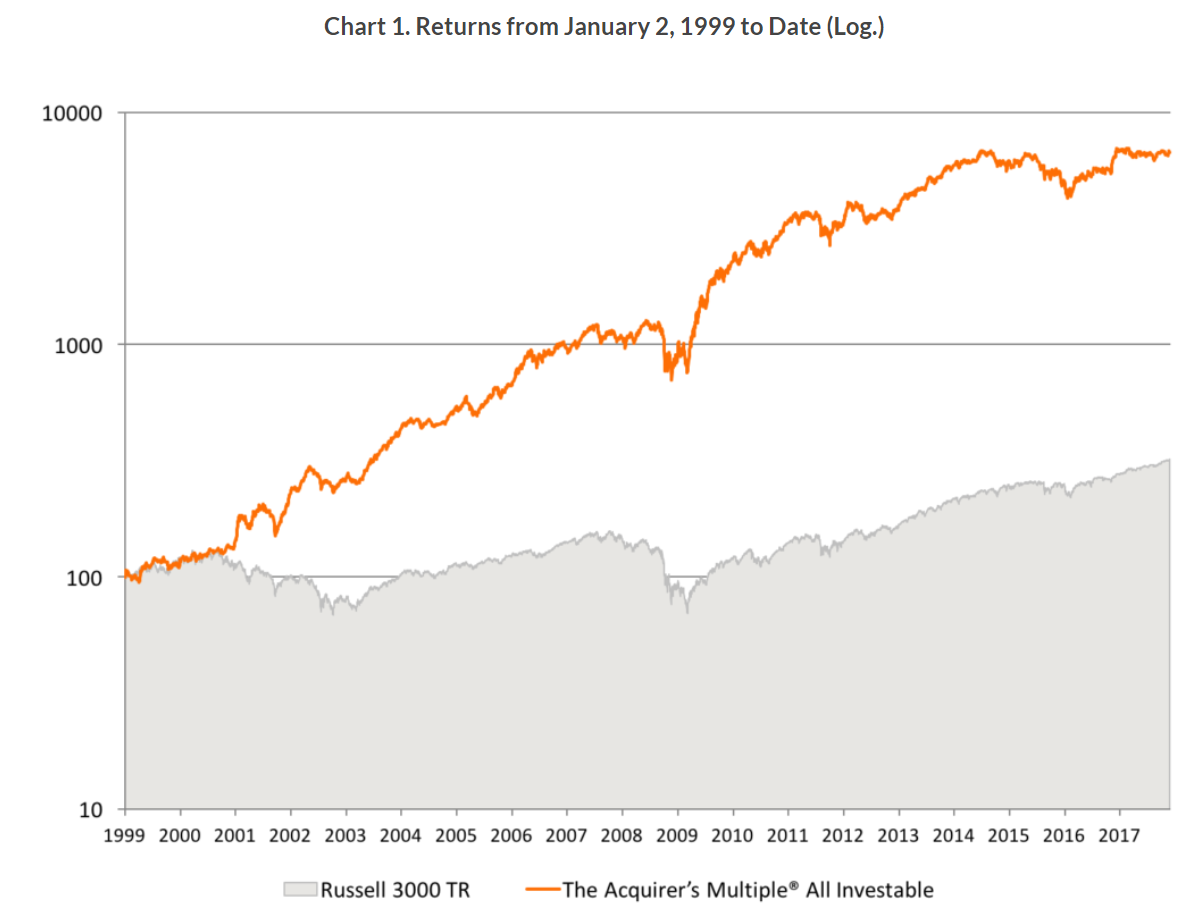

On Carlisle’s site, he offers up some data on how a concentrated portfolio holding the top ranked (i.e. cheapest) stocks based on the Acquirer’s Multiple would have performed going back to 1999. The chart below shows the long term compounded return of the All Stocks portfolio compared to the Russell 3000 index. The portfolio, which consists of the top 30 stocks based on the Acquirer’s Multiple, is re-balanced annually and at the time of each re-balancing the top scoring stocks are added into the portfolio. This effectively refreshes the holdings so that the cheapest, most attractive stocks based on the most recent fundamentals are held. There may be additional filters applied to the screen. For instance, screening out firms with possible earnings manipulation or that are in financial distress appears to be accomplished via additional quantitative methods, but the key selection criteria is the Acquirer’s Multiple.

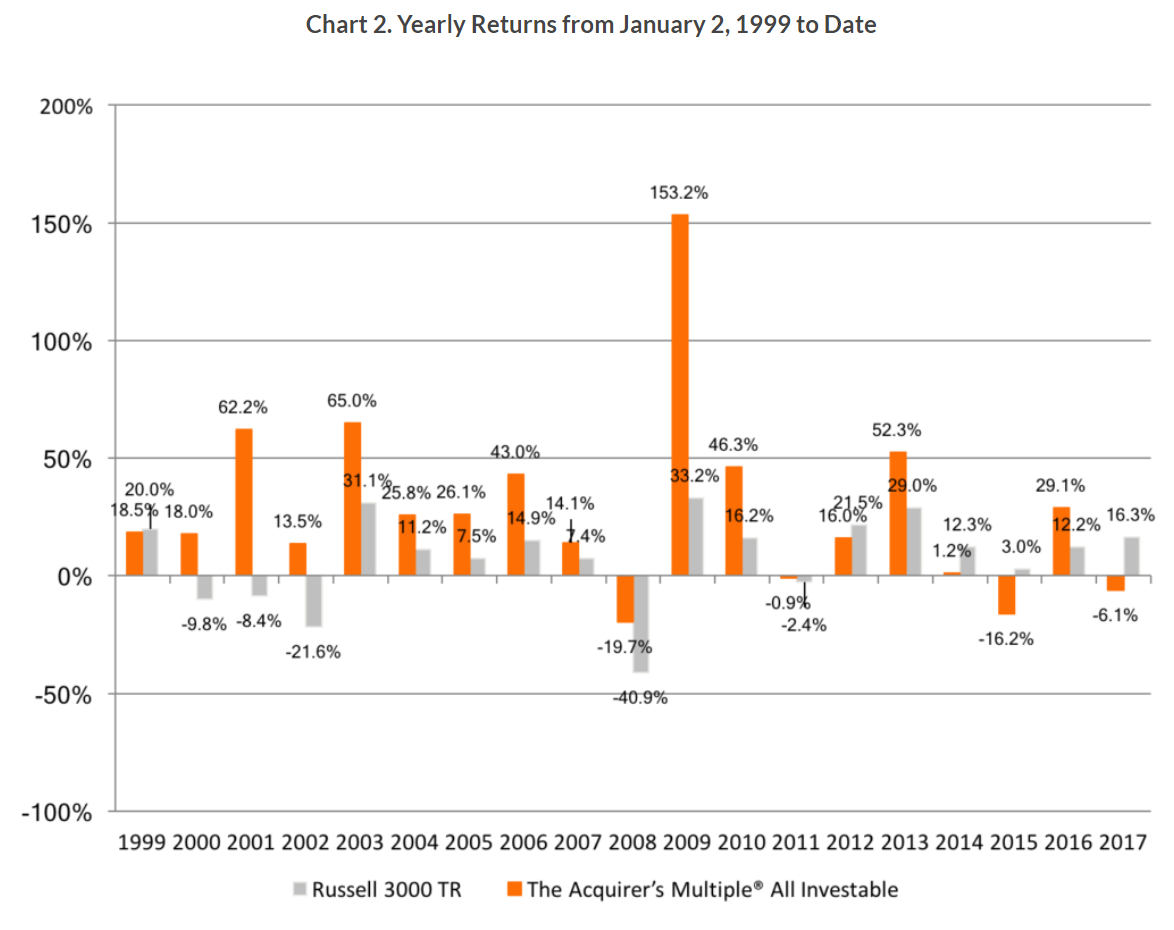

As you can see from the chart, the back test shows significant outperformance over the market from 1999 through late 2017. The period of 1999 to mid-2007 was very strong for value stocks, and the portfolio showed substantial relative outperformance during that period. In 2008, the portfolio only declined half that of the market, which would have been excellent for a deep value approach during that period. Then coming out of the financial crisis, the portfolio ripped higher and returned nearly 5x that of the market in 2009. The second chart shows that the big up years (2003, 2009, 2013) are very important, as performance for this type of strategy typically comes in spurts. Keep in mind, this is a back test and not an actual money management track record, but the results show something very important, which is that strategies like this can have huge up years and in order to give yourself the chance for market beating returns such as these, you have to stay in the game and invested in the strategy. Those massive up years are nearly impossible to predict beforehand, which is why taking a long-term perspective is key to one’s success when investing in a model like this.

Like all investment strategies, there have been years of underperformance, most notably 2012, 2014 and 2015. That is consistent with our implementation of the Acquirer’s Multiple as well and is to be expected during periods where value struggles. In our testing, a focused 10 stock portfolio that is rebalanced tax efficiently has generated market beating returns, backing up Carlisle’s research.

Source: https://acquirersmultiple.com/2015/01/all-investable-stock-screen-backtest/

A List Of Value Names

Below is a list of the current top-rated stocks using our model based on Carlisle’s Acquirer’s Multiple. None of these should be construed as investment recommendations in isolation. The list is presented to provide an idea of the type of stocks this model selects.

| Ticker | Name | Mkt Cap ($mil) | Sector | Industry | Acquirers Multiple |

| TTM | TATA MOTORS LIMITED | $16,579 | Consumer Cyclical | Auto & Truck Manufacturers | 3.96 |

| UTHR | UNITED THERAPEUTICS CORP | $4,802 | Healthcare | Biotechnology & Drugs | 5.39 |

| TX | TERNIUM SA | $6,539 | Basic Materials | Iron & Steel | 5.39 |

| ABX | BARRICK GOLD CORP | $14,370 | Basic Materials | Gold & Silver | 5.59 |

| MCK | MCKESSON CORPORATION | $31,432 | Healthcare | Biotechnology & Drugs | 5.62 |

| LPL | LG DISPLAY CO LTD. | $9,434 | Technology | Electronic Instr. & Controls | 5.90 |

| AUO | AU OPTRONICS CORP | $4,512 | Technology | Electronic Instr. & Controls | 6.14 |

| TECK | TECK RESOURCES LTD | $15,744 | Energy | Coal | 6.29 |

| STO | STATOIL ASA | $76,919 | Energy | Oil & Gas Operations | 6.41 |

| E | ENI SPA | $62,961 | Energy | Oil & Gas Operations | 6.83 |

| NGLOY | ANGLO AMERICAN PLC | $34,643 | Basic Materials | Metal Mining | 6.94 |

| ALK | ALASKA AIR GROUP, INC. | $8,180 | Transportation | Airline | 7.00 |

| RIO | RIO TINTO PLC | $94,006 | Basic Materials | Metal Mining | 7.03 |

| LPX | LOUISIANA-PACIFIC CORP | $4,299 | Capital Goods | Constr. – Supplies & Fixtures | 7.11 |

| DAL | DELTA AIR LINES, INC. | $40,075 | Transportation | Airline | 7.20 |

| AA | ALCOA CORP | $8,793 | Basic Materials | Metal Mining | 7.24 |

| M | MACY’S INC | $8,802 | Services | Retail (Department & Discount) | 7.26 |

| HTHIY | HITACHI, LTD. | $35,902 | Technology | Electronic Instr. & Controls | 7.44 |

| MGA | MAGNA INTERNATIONAL | $19,992 | Consumer Cyclical | Auto & Truck Parts | 7.49 |

| MT | ARCELORMITTAL SA | $33,502 | Basic Materials | Iron & Steel | 7.56 |

Finding value stocks in what looks like a pricey market can sometimes be difficult, but the Acquirer’s Multiple offers investors a good, and relatively straight-forward way to find companies that are trading at attractive values relative to their earnings. Add on to it that the strategy has been proven over time, and its easy to see the appeal of this Ben Graham inspired quantitative value model.

Justin J. Carbonneau is Partner at Validea Capital Management and Validea.com. You can follow Justin on Twitter @jjcarbonneau.