A paper published last month by GMO argues that the market’s current elevated valuations should not be blamed solely on the technology sector. Still, it says the market is expensive “no matter how you cut it.”

Here are some highlights;

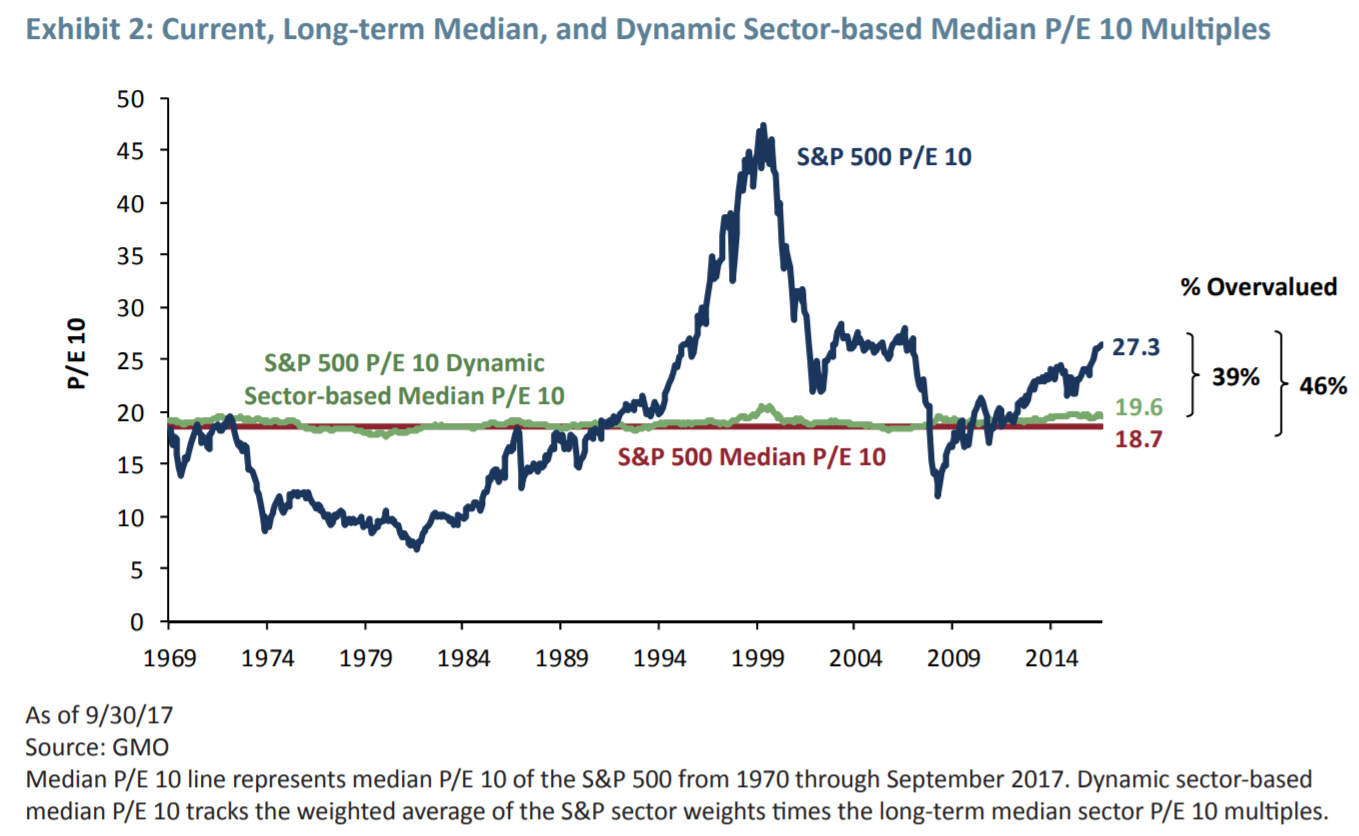

The paper provides data showing how the shift to “higher-multiple sectors” only accounts for a portion of today’s pricier market (P/E 10 is also known as the Shiller PE or cyclically adjusted price-earnings-ratio):

GMO suggests that comparing today’s market P/E to the long-term median level might not be the best approach given the changing sector composition as it “makes the assumption that the level the S&P 500 traded at on average in the past is ‘fair’ today.” Explaining that the green line in the above graph represents a possible long-term, sector-weighted value multiple of the S&P 500 (19.6), the paper suggests that while some of the elevated market P/E is sector-based, “it is hardly enough to call the S&P 500 fairly valued.”

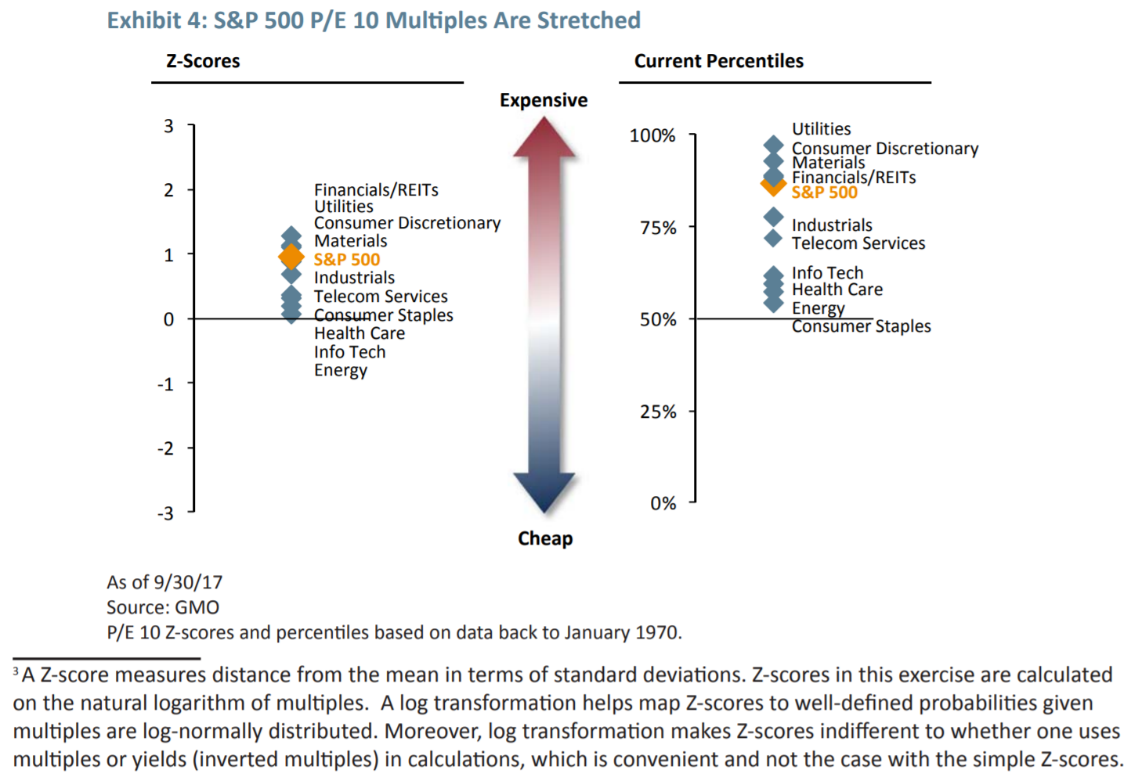

It also argues that while on a standard deviation basis, current valuations are “not too extreme,” on a percentile basis they are “among the most expensive we’ve seen dating back to 1970:”

Technology sector is cause for some of its expensiveness (both vs. history and other developed markets), but it does not explain away the bulk of its high absolute and relative valuation level.”